OUR COMPANY

OUR COMPANY

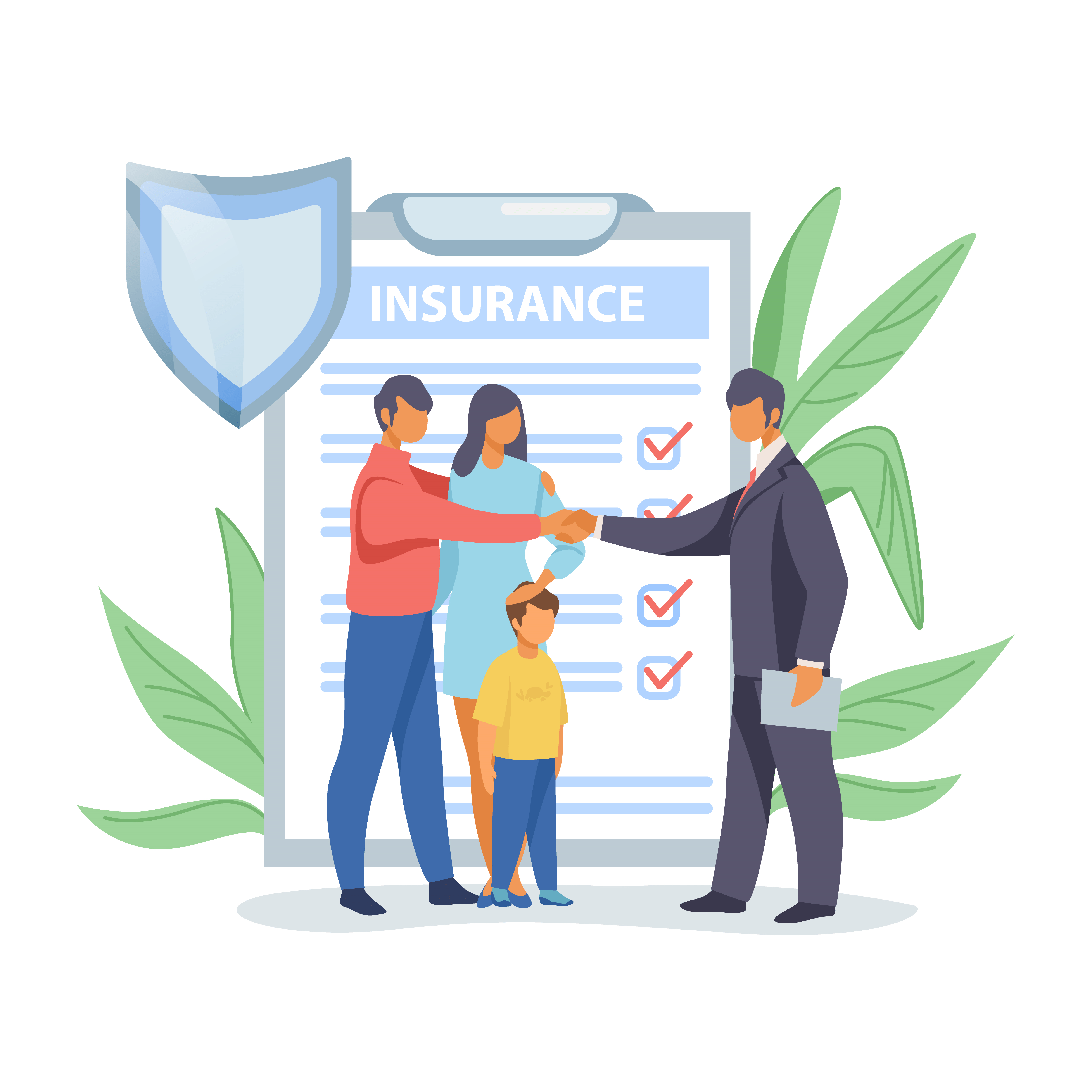

An individual mediclaim policy ensures that only the designated individuals enjoy its exclusive benefits.

A family floater mediclaim policy allows the insured to extend coverage benefits to their entire family.

Safeguards against accidental death and both permanent and temporary disabilities.

Offers enhanced coverage at a cost-effective premium, supplementing your existing health insurance.

A comprehensive mediclaim insurance plan designed for Indian residents and expatriates living in India for at least one year.

Insurance plans that specifically cover accidental hospitalization along with personal accident coverage, offered at an affordable premium.

Get Cashless Treatments in 10000+ Network Hospitals

Covers expenses for private rooms, wards, or ICU during hospitalization.

Covers expenses for doctor’s consultations, including specialist visits.

Include expenses such as oxygen cylinders, blood, organ donation, diagnostic tests, and more.

Requires less than 24-hour hospitalization, IFFCO-TOKIO covering up to 380 treatments.

Medical expenses for up to 60 days before hospitalization and 90 days after are included.

Includes treatments like Ayurveda, Yoga, Naturopathy, Unani, Siddha, and Homeopathy.

Coverage includes ambulance expenses for medical emergencies.

The sum insured is refilled after a claim, allowing you to use the coverage again-usually with an extra premium.

Includes coverage for advanced procedures such as robotic surgery, stem cell therapy, and more.

Procedures for enhancing appearance rather than addressing life-threatening conditions are not covered.

Injuries resulting from self-inflicted harm are excluded from policy coverage.

Injuries from adventure sports, war, or nuclear explosions are not covered.

Disclaimer: For detailed information about coverage and exclusions, please refer to the policy wording document.

You can choose any hospital room without any cap on room rent.

Your sum insured doubles if you're diagnosed with a life-threatening illness.

Covers treatment essentials like gloves, syringes, masks, and more.

Get benefits like free teleconsultations, discounted services, rewards, and renewal discounts.

Covers natural events like pregnancy and childbirth.

Covers dental care like root canals, extractions, fillings, and preventive treatments.

Covers OPD consultations and diagnostic services.

Our customers have rated us

Based on 2378 reviews

I chose this essential health insurance plan because it offers wide coverages like dental, maternity and more.

Their family health insurance policy covers me, my spouse, and kids, all in one plan. Very helpful!

Very transparent and reliable insurance provider.

I’m happy they included pre-existing disease coverage after a short waiting period.

The policy even has a room rent waiver, which saved us a lot during hospitalization.

Great customer satisfaction.

In the purview of the sedentary lifestyle, people are at a high risk of suffering from various diseases. Purchasing a medical policy can help you get financial assistance in the hour of need. Today, a lot of people prefer buying a mediclaim health insurance policy because of the following reasons :

Mediclaim insurance provide protection against medical bills

You can avail of the cashless facility at network hospitals

Mediclaim is available for both individual and family

It provides tax benefits on the annual premium

Prefer face-to-face assistance? Our branches offer expert guidance during office hours. But for a faster, hassle-free experience, buy your Mediclaim policy online and enjoy these benefits:

Skip the traffic and long queues! In just three simple steps, get instant coverage against medical emergencies, all from the comfort of your home.

No travel, no waiting. The online process takes just a few minutes, ensuring quick access to the coverage you need.

Buy your policy anytime, anywhere, even on a Sunday afternoon or a public holiday. Online access is available 24/7.

No lengthy paperwork! Simply enter your details, upload documents, and receive your policy instantly via email.

Your payments are processed through a secure gateway, ensuring your credentials remain protected.

Download Policy Documents

(Prospectus / Sales Literature / Policy Wording /Proposal Form / Claim Form / Customer Information Sheet (CIS) etc.)

Popular Searches

Download App

Lets Connect