OUR COMPANY

OUR COMPANY

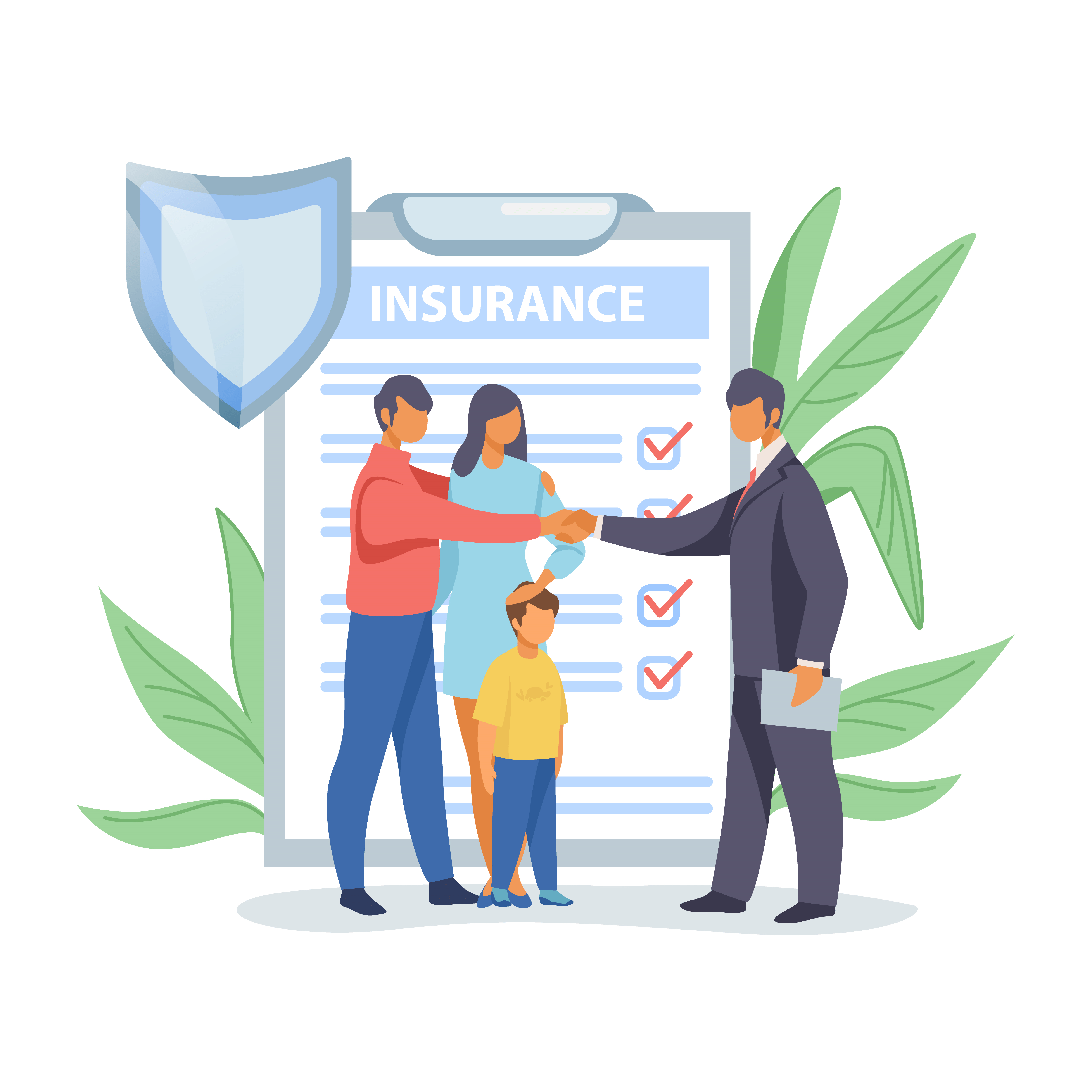

Family Health Insurance

Buy/Renew Family Floater Health Insurance Policy Online

Family Health Insurance also known as a ‘Floater Plan', is like an umbrella that protects your whole family under one policy only. The sum insured is shared among all the insured family members and can be used when the need arises.

Many people question the value of family health insurance. The answer is simple: Family health insurance plans provide comprehensive medical coverage for your entire family, safeguarding them from a wide range of health issues. But that's not all! Family health insurance offers additional benefits that go beyond just financial protection in case of an emergency. Keep reading to explore the advantages of having a family health insurance plan.

A single plan protects your entire family (spouse, children) against medical emergencies and gives financial protection to the whole family under one plan.

As compared to an individual health insurance policy, family plans have a much higher sum insured. This ensures a higher level of protection for your loved ones.

Premiums are generally lower for family health insurance plans compared to buying individual plans for each family member.

It is easy to manage one plan for the whole family as it simplifies the renewal and claim processes.

In case of medical emergencies, this plan protects your savings from being wiped out by unexpected medical bills for any of the insured family members.

You can avail of tax deductions on premiums paid for family health insurance and save up to ₹ 1,00,000 under Section 80D of the Income Tax Act.

Knowing your family is protected from medical expenses provides peace of mind and allows you to focus on their well-being rather than stressing about the uncertainties of life.

You can easily include new members of your family in the family medical insurance plan. You don’t have to go through too many formalities, and it’s much simpler than getting a new individual plan.

Few reasons to consider IFFCO Tokio Health Insurance :

Instant Quote

Easy Renewals

Simple Process

Instant Policy Issuance

Reliable 24*7 Support

Personalized plans

High Claim Settlement Ratio

Secure Payments

Our customers have rated us

Based on 2378 reviews

I chose this essential health insurance plan because it offers wide coverages like dental, maternity and more.

Their family health insurance policy covers me, my spouse, and kids, all in one plan. Very helpful!

Very transparent and reliable insurance provider.

I’m happy they included pre-existing disease coverage after a short waiting period.

The policy even has a room rent waiver, which saved us a lot during hospitalization.

Great customer satisfaction.

| Key Features | Benefits of IFFCO Tokio |

|---|---|

| Sum Insured | Up to Rs. 30 lakhs |

| Room Rent Charges Covered | Up to actuals |

| ICU Charges Coverage | Up to actuals |

| Ambulance Charges Coverage | Up to Rs.2,500 |

| Daily Allowance Coverage | Up to Rs.1,000 per day |

| Co-pay | Nil |

| Critical Illness | Covered |

| No medical test | Upto 60 years |

| Reinstatement Benefit | Available |

| Day Care Cover | 380+ procedures covered |

| Online Renewal | Available |

| Lifelong Renewal | Yes |

| Tax Benefit under 80D | Upto 1 Lakh |

| Cashless Treatment | Available at 8000+ hospitals |

| COVID-19 Treatment | Covered |

| Claim Assistance | With 24/7 customer service |

| Pre Hospitalization Expenses | Upto 60 Days |

| Post Hospitalization Expenses | Upto 90 Days |

| Nursing Expenses | Covered |

| Wellness Benefits | Covered |

Get Cashless Treatments in 8000+ Network Hospitals

It’s our responsibility to protect our family from uncertainties without having to worry about finances. With the IFFCO Tokio Family Health Insurance Plan, you can rest assured that your loved ones are protected against unfortunate events. The coverage benefits that you get with us are as follows-

Our family health insurance covers more than 380 Day Care Surgeries.

Hospitalization charges including Room Rent Expenses, Surgical Expenses, Registration etc.

Includes pre and post-hospitalization medical expenses for true peace of mind.

Health Check-ups & Vaccination expenses are included with Family Health Insurance.

Health Insurance cover expenses for treating critical illnesses.

Our Family Health Insurance Policy covers ambulance service.

Our Family Health Insurance covers AYUSH treatments.

Our Family Health Insurance covers Laboratory Services.

Room Rent Waiver- Get a hospital room as per your requirement, with no limit on room rent.

Consumables- Treatment essentials like syringes, masks, bandages, etc., are covered with this add-on.

Wellness Benefit- Avail valuable benefits like e-pharmacy, yoga sessions, and rewards along with discounts on renewal.

Critical Illness- Your sum insured gets doubled in case you get diagnosed with a life-threatening illness to help you manage treatment costs.

It is our constant effort to provide your family with comprehensive protection from medical exigencies and ultimate protection. Every family health insurance policy will have a set of limitations. These exclusions refer to medical conditions and expenses that are not covered by the family medical insurance policy. These usually include, but are not limited to:

Any procedure that does not address any medical condition but aims to improve one’s appearance will not be covered under your family health insurance plan.

Dental care, including surgeries or implants, often focuses on preventive measures like cleanings and check-ups.

Childbirth and pregnancy are considered natural events and not medical problems. Hence, such conditions are not covered under your policy.

A health insurance plan for your family will not cover any self-inflicted injuries.

Any medical emergency arising due to war, adventurous sports, a nuclear explosion, etc., is considered outside the scope of health insurance, and your policy will not provide coverage for such events.

Buying health insurance for your family is important, but selecting the right plan that would benefit all family members is even more important. We have listed a few key factors that you should consider before making the final purchase of your family health insurance plan.

There can be some factors which can impact your eligibility to buy a family health insurance plan-

To buy a health insurance plan, your age should be between 18 and 60 years.

Our policy covers Indian nationals residing in India only.

Any pre-existing medical conditions including chronic illness or any disorder would impact the coverage of your plan and may have varying waiting period.

If you have any habits like smoking or alcoholism that can negatively impact your well-being, then both your eligibility and premium rate will be affected.

If your job is risky in nature, you might have some specific eligibility criteria.

When you buy a family medical insurance plan online, you can enjoy multiple benefits. A few benefits are:

You can buy the family health insurance policy online from our website within a few minutes by making a few clicks on your laptop or mobile device.

You do not have to physically visit the branch or adhere to our office hours. You can also buy a family medical insurance plan while at the office, at home, or while you are traveling.

One of the best things about buying a family medical insurance plan online is that you get instant access to your policy as soon as you make the payment.

Our health insurance experts are always happy to answer all your medical insurance-related queries so that you can choose the right plan.

Every minute detail relating to your policy is made available to you so that you are able to make an informed decision.

Your payments are processed via a secure gateway, ensuring your credentials remain protected.

The process of purchasing a family health insurance plan is quite simple; all you have to do is follow these simple steps.

You can enjoy a quick renewal of your policy by simply visiting our website and filing a claim online.

Renewing your policy online has simple steps and a user-friendly interface to make the renewal process smooth and straightforward.

You can renew your family health insurance policy from anywhere. You just need an internet connection, and within minutes, you’ll have your policy renewed without contacting any agents or visiting a branch in person.

You can make the payment via our secure payment gateways using multiple modes like credit card, debit card, net banking, wallets, UPI, etc.

Regardless of our business hours, the online policy renewal portal is accessible and available to you anytime of the day or night.

Online renewals eliminate the paperwork and make the whole process environment-friendly.

You can renew your family health insurance via following simple steps –

Download Forms

Popular Searches

Download App

Lets Connect